23 Apr 2026

Freelancer Account vs. Corporate Account: Which One Should You Choose?

As your business grows, so does the complexity of your finances. In the world of 2026, the line between a solo professional and a small corporation is often thin, but the bank account you choose can make or break your operational efficiency. At Credits.com, we offer both Freelancer and Corporate accounts, but they are built for very different stages of the business journey.

Here is how to decide which one fits your current reality and when it’s time to scale up.

The Freelancer Account: Designed for the Solo Professional

If you are a "Business of One"-a developer, designer, or consultant operating under your own name or a simple sole proprietorship-the Freelancer account is your starting point.

Who it is for:

Solo contractors working for multiple international clients.

Digital nomads who need to receive payments in USD or EUR while living in a third country.

Professionals who need a dedicated IBAN to separate personal spending from business income.

Key Benefits:

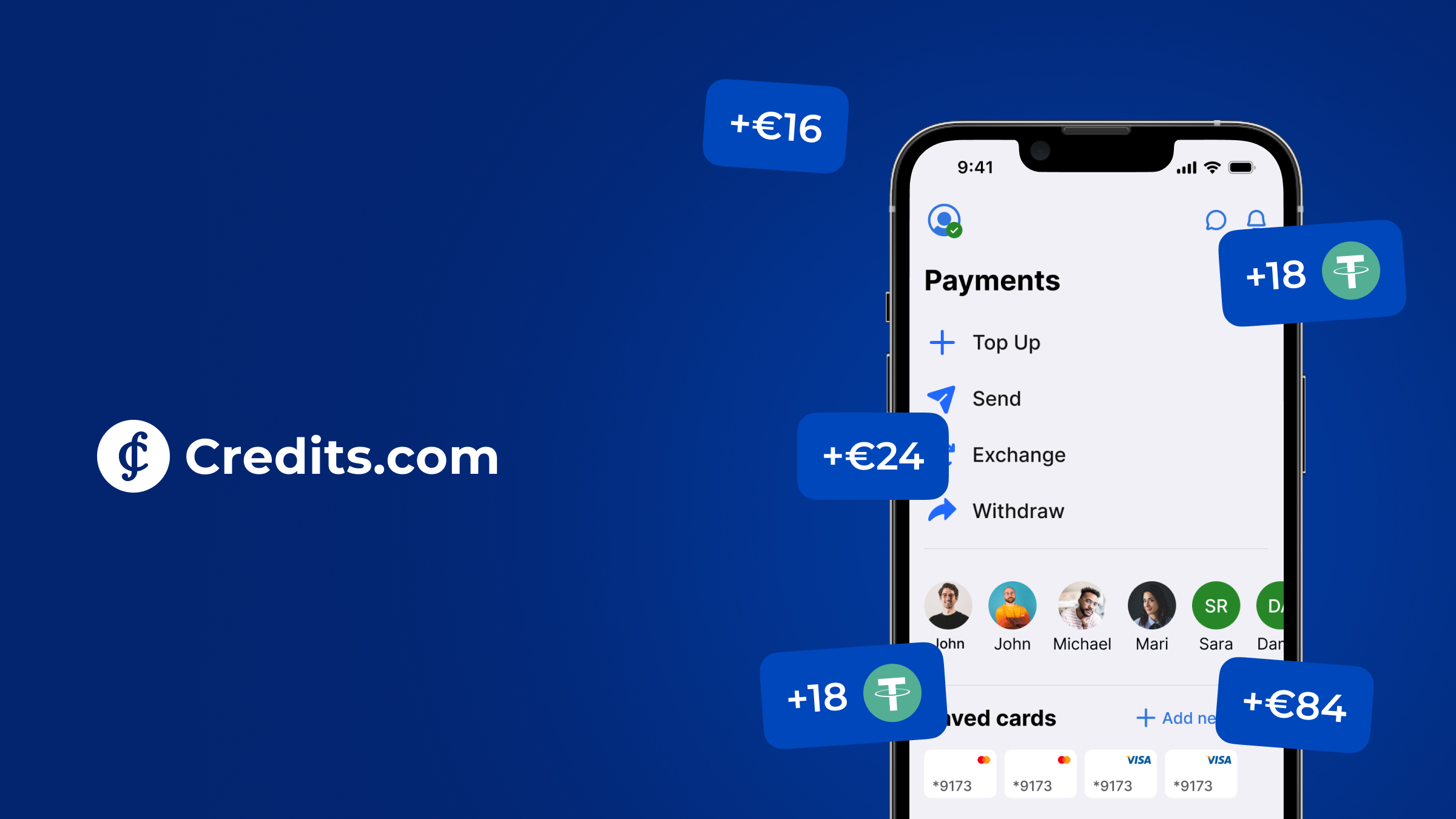

Ease of Onboarding: The verification process is streamlined for individuals. You get your IBAN faster because the compliance checks (KYC) are focused on you, not a complex legal entity.

Multi-Currency Versatility: Just like our individual accounts, you get access to 20+ currencies. You can receive a USD payment from a US client and spend it in EUR via your Credits card without massive conversion fees.

Lower Barrier to Entry: Typically, these accounts have lower monthly maintenance costs (or are even free on the Standard tier), making them ideal for those just starting their journey.

The Corporate Account: Designed for Scalability and Legal Entities

Once you incorporate (LLC, Ltd, GmbH, etc.), a Freelancer account is no longer enough. You need a setup that recognizes your business as a legal person, separate from your personal identity.

Who it is for:

Registered companies with one or more employees.

Businesses engaged in high-volume cross-border trade (importers/exporters).

Any entity that needs to hold funds in the company’s name for tax and legal compliance.

Key Benefits:

Higher Limits: Corporate accounts come with significantly higher transaction and holding limits. If you are moving six-figure sums for inventory or payroll, this is the only way to go.

Custom Workflows: Our International and Custom Business Plans allow for tailored fees and dedicated support. You aren't just an "user"; you are a partner with a dedicated manager.

B2B Trust: Sending an invoice from a registered corporate entity with a corresponding corporate IBAN builds immediate trust with large vendors and government tax offices.

Bulk Payouts: If you need to pay a team of 10 freelancers across 30 different currencies, the Corporate account’s batch payment features and LPM/APM (Local Payment Methods) integrations save hours of manual work.

When Should You Switch?

Choosing the right account is about timing. If you stay on a Freelancer account for too long, you hit a "ceiling." If you move to Corporate too early, you might pay for features you don't yet use.

Switch to a Corporate Account if:

You Have Incorporated: Legally, your business income should flow into an account owned by the entity, not the individual.

You are Hiring: Once you have a team, you need a system that can handle payroll and multiple cards for employees.

You Hit Transaction Limits: If your bank starts flagging your incoming transfers because they exceed "personal" thresholds, it’s a clear signal to move to a Business plan.

You Need Custom Pricing: When your volume reaches a certain point, the 0.4%–0.6% SEPA/SWIFT fees on our standard plans can be negotiated into a custom package that fits your specific margins.

Why Credits.com for Both?

Whether you are a solo dev or a CEO of a global trading firm, Credits.com provides the same core "Super App" advantage:

Unified Dashboard: See your fiat and crypto balances in one place.

Transparent Rates: No hidden FX markups.

The Crypto Bridge: Use stablecoins to settle international invoices 24/7 when traditional banks are closed.

Start with a Freelancer Account if you are building your personal brand and need speed. Move to a Corporate Account the moment your business becomes a legal entity or your transaction volume demands professional-grade limits. At Credits.com, we scale with you-ensuring that no matter how big you get, your banking friction stays small.